Starting a business usually brings one big question very quickly:

How will you pay for it?

Some businesses can start with almost no money. Others need equipment, inventory, software, a website, marketing, legal setup, staff, product development, or a physical location before they can open.

That is where funding becomes important.

But not every funding option works the same way.

The three most common paths are:

Bootstrapping

Business loans

Investors

Each one has advantages. Each one has risks. Each one changes how you build your business.

The right option depends on your business model, your costs, your risk tolerance, your growth plans, and how much control you want to keep.

This guide explains the difference between bootstrapping, loans, and investors in simple language.

It is not personal financial advice. It is a beginner-friendly overview to help you understand your options before making serious funding decisions.

Affiliate disclosure: This post contains affiliate links. If you make a purchase through one of these links, ProBusinessStrategy may earn a small commission at no extra cost to you. We only recommend tools we genuinely believe in.

What Is Business Funding?

Business funding means finding the money or resources needed to start, operate, or grow a business.

That money may come from your own savings, early customer payments, bank loans, credit lines, crowdfunding, grants, friends and family, angel investors, venture capital, or business revenue.

But at the beginning, most entrepreneurs face three main choices:

Use your own resources.

Borrow money.

Give up part of the business in exchange for capital.

Those three choices are the foundation of bootstrapping, loans, and investors.

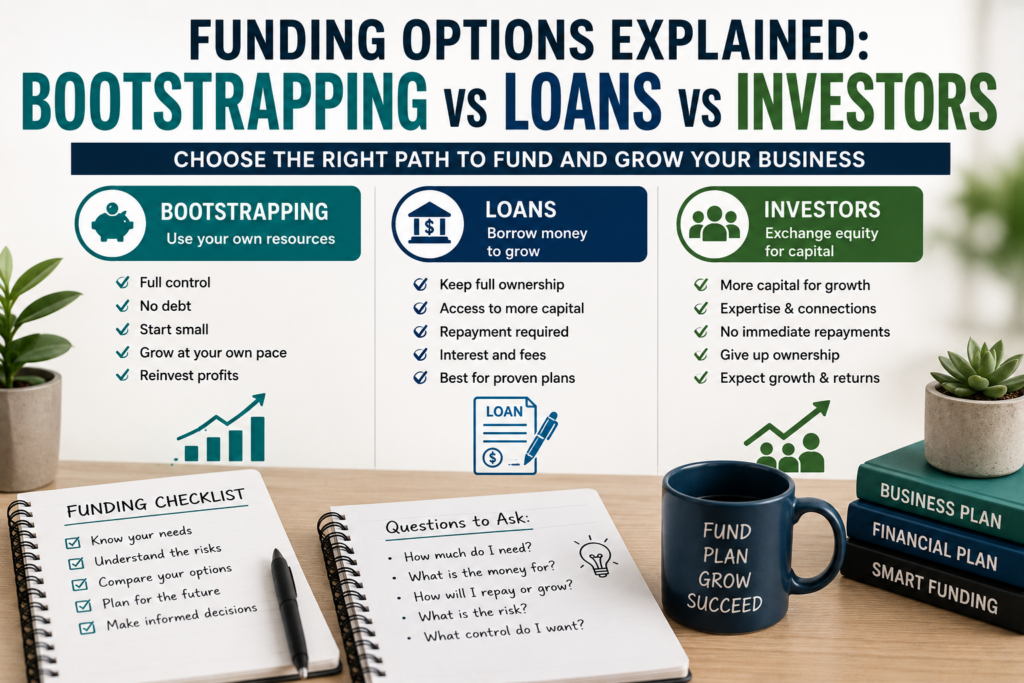

Option 1: Bootstrapping

Bootstrapping means building your business mostly with your own resources.

This may include:

Personal savings

Income from a job

Early customer payments

Pre-orders

Small profits reinvested into the business

Low-cost tools

Working from home

Doing the work yourself

Starting small before expanding

Bootstrapping is often the simplest way to begin because you do not need lender approval or investor permission.

You start with what you have.

This is common for freelancers, consultants, online businesses, service businesses, bloggers, affiliate marketers, digital product sellers, small e-commerce experiments, and home-based businesses.

The Main Advantage of Bootstrapping

The biggest advantage is control.

When you bootstrap, you usually keep full ownership of the business.

You decide what to build, how fast to grow, what customers to serve, how much to charge, and when to change direction.

You also avoid taking on debt too early.

That can make bootstrapping attractive for beginners who want to learn without heavy financial pressure.

Another advantage is discipline.

When money is limited, you are forced to focus on what matters:

Getting customers

Solving real problems

Keeping costs low

Testing before spending

Making revenue early

This can create a healthier business mindset.

The Main Disadvantage of Bootstrapping

The biggest disadvantage is slower growth.

If you only use your own money and early revenue, you may not be able to move as fast.

You may not be able to hire help, buy inventory, build technology, advertise, or expand quickly.

Bootstrapping can also create personal pressure.

If you use your savings, work long hours, and do everything yourself, the business may become stressful.

Bootstrapping works best when the business can start small and generate revenue early.

It is harder when the business needs a large amount of money before it can operate.

When Bootstrapping Makes Sense

Bootstrapping may be a good fit when:

Startup costs are low

You want to keep ownership

You can start from home

You can sell a service first

You can test before building

You do not need inventory immediately

You want to grow slowly and carefully

You want to avoid debt

You are still validating the idea

Examples:

A freelance writing business

A consulting service

A home-based design studio

A blog or affiliate website

A digital product shop

A coaching business

A virtual assistant service

A small online course business

For many beginners, bootstrapping is the safest first step because it allows them to test the business before making a bigger financial commitment.

Option 2: Business Loans

A business loan means borrowing money that you agree to repay.

The loan may come from a bank, online lender, credit union, government-backed program, microloan provider, or other financing source.

Loans can be used for many business needs, such as:

Equipment

Inventory

Startup costs

Working capital

Marketing

Renovation

Hiring

Technology

Cash flow

Expansion

The important difference is this:

With a loan, you do not usually give up ownership.

But you do take on repayment responsibility.

The Main Advantage of Loans

The biggest advantage of a loan is that you can access money without selling part of your business.

If you borrow money and repay it properly, you may keep full ownership.

This can be useful when the business has a clear plan for using the money.

For example, a loan may make sense if you need equipment that helps you serve customers, inventory that you already know can sell, or working capital for a business with predictable demand.

Loans can also help a business grow faster than bootstrapping alone.

The Main Disadvantage of Loans

The biggest disadvantage is repayment pressure.

A loan must usually be repaid whether the business succeeds quickly or not.

That can be risky for beginners.

If revenue is slower than expected, loan payments can become stressful.

Loans may also require:

Good credit

Business history

Collateral

Financial documents

A business plan

Personal guarantees

Proof of revenue

Clear repayment ability

Not every new business will qualify.

And even if you qualify, that does not mean borrowing is automatically wise.

Borrowed money should have a clear purpose.

When Loans Make Sense

Loans may make sense when:

You know exactly what the money is for

The business model is already tested

You have predictable revenue

The loan helps create more income

You understand the repayment terms

You can handle the risk

You do not want to give up ownership

Examples:

Buying equipment for a profitable service business

Purchasing inventory for an already tested product

Expanding a business with proven demand

Funding working capital for a business with regular sales

Improving operations for a business that already has customers

Loans are usually better for businesses with some clarity, not only an idea.

If you are still unsure whether the business works, bootstrapping or small experiments may be safer first.

Option 3: Investors

Investors provide money in exchange for something.

Usually, that means equity: a percentage of ownership in the company.

In some cases, investment can also involve convertible notes or other agreements that may later turn into equity.

Investors are most common in startups that have strong growth potential.

This may include software companies, technology startups, scalable marketplaces, product businesses, platforms, apps, biotech, fintech, or other businesses that can grow quickly.

Investors are usually not looking for small lifestyle businesses.

They want businesses that can become much larger.

The Main Advantage of Investors

The biggest advantage is access to growth capital without immediate loan repayment.

Unlike a loan, investor money usually does not require monthly repayments in the same way.

That can give a startup more room to build, hire, test, develop, and grow.

Investors may also bring:

Experience

Connections

Credibility

Strategic advice

Industry knowledge

Future funding access

A good investor may help open doors that money alone cannot.

The Main Disadvantage of Investors

The biggest disadvantage is giving up ownership and some control.

When you take investor money, you may no longer own the whole business.

You may also have more pressure to grow fast.

Investors usually expect a return.

That means the business may need to aim for a larger outcome than the founder originally planned.

This can change the nature of the business.

A founder who wants a simple, profitable, independent business may not enjoy investor pressure.

Investment is not free money.

It is a serious business relationship.

When Investors Make Sense

Investors may make sense when:

The business can scale quickly

The market opportunity is large

You need capital before revenue

Growth speed matters

You are comfortable sharing ownership

You want to build a company that can become much bigger

You understand investor expectations

You have a strong pitch and growth plan

Examples:

A software startup

A marketplace platform

A high-growth product company

A technology company

A scalable B2B tool

A startup with strong network effects

A business that needs major upfront development

Investors are usually not the best fit for every small business.

They are best for businesses designed for scale.

Bootstrapping vs Loans vs Investors

The simplest way to understand the difference is this:

Bootstrapping uses your own resources.

Loans use borrowed money.

Investors use outside capital in exchange for ownership or future upside.

Each path creates a different type of pressure.

Bootstrapping creates resource pressure.

Loans create repayment pressure.

Investors create growth and ownership pressure.

The best funding option is not always the one that gives you the most money.

It is the one that matches the business you are trying to build.

Compare the Three Options

Bootstrapping gives you control, but may limit speed.

Loans give you capital without giving up ownership, but create repayment obligations.

Investors can help you grow faster, but you may give up equity and control.

A small home-based business may not need investors.

A local service business may use bootstrapping first and a loan later.

A software startup may need investors if the product takes a long time to build before revenue.

A digital product business may be bootstrapped almost completely.

An e-commerce business may bootstrap testing, then use financing for inventory once demand is proven.

The business model matters.

The Wrong Way to Choose Funding

A common mistake is asking:

“How can I get money?”

A better question is:

“What type of funding fits this business model?”

Many beginners want funding because they think money will solve uncertainty.

But money does not fix a weak idea.

Money does not prove demand.

Money does not create customers by itself.

Before looking for funding, ask:

Do people want this?

Can I sell it?

What does it cost to deliver?

How much money do I actually need?

What will the money be used for?

How will the business make the money back?

What risk am I taking?

What control am I giving up?

Funding should support a clear business plan, not replace one.

Start With the Smallest Test

Before borrowing money or looking for investors, try to test the idea in the smallest possible way.

Examples:

Sell the service manually first

Create a simple landing page

Take pre-orders

Offer a paid pilot

Create a small prototype

Test content on social media

Talk to potential customers

Run a small local test

Create a basic version of the product

This helps you learn before you spend heavily.

If the test works, you have stronger evidence.

If it fails, you have saved money.

This is especially important for new entrepreneurs.

The first version of a business idea is often not the final version.

Testing gives you information before you commit.

Create a Simple Funding Plan

A funding plan does not need to be complicated.

Start with these questions:

What do I need money for?

How much do I need?

When do I need it?

Can I start smaller?

Can I earn before I spend?

Can customers pay upfront?

Can I reduce costs?

Can I use revenue to grow?

Would debt be manageable?

Would investors be appropriate?

Write the answers down.

You may discover that you do not need as much money as you thought.

Or you may discover that the business needs more planning before it is ready for funding.

Funding Examples

Example 1: Home-Based Service Business

A person wants to start a virtual assistant business from home.

Startup costs may include a laptop, internet, website, basic branding, scheduling tool, and marketing.

This business may not need a loan or investor.

Bootstrapping makes sense because the founder can start with low costs, find clients, and reinvest profits.

Example 2: Local Food Business

A person wants to open a small food shop.

This may require equipment, permits, inventory, rent, renovation, insurance, and staff.

Bootstrapping alone may not be enough.

A loan may be considered if the founder has a strong plan, understands costs, and has a realistic path to revenue.

Example 3: Software Startup

A founder wants to build a complex software platform.

The product may require developers, design, testing, marketing, and time before revenue.

If the market is large and the growth potential is strong, investors may make sense.

But if the product can be built in a smaller version first, bootstrapping a simple prototype may still be the first step.

Example 4: E-Commerce Business

A person wants to sell physical products online.

The founder may start by testing demand with a small product batch, pre-orders, dropshipping, print-on-demand, or affiliate content.

If demand is proven, funding may later help buy inventory or improve operations.

This is often better than borrowing money before knowing whether people want the product.

Helpful Support Before Seeking Funding

Before applying for a loan or talking to investors, you may need a business plan, financial projection, pitch deck, market research, or simple spreadsheet.

If you do not want to create everything yourself, Fiverr can be useful for finding freelancers who offer business plan writing, pitch deck design, financial model templates, market research, bookkeeping templates, and startup presentation design.

This does not replace professional financial or legal advice.

But it can help you organize your materials before speaking with lenders, investors, advisors, or potential partners.

Do Not Forget Grants and Crowdfunding

Bootstrapping, loans, and investors are the main comparison in this article, but they are not the only options.

Some businesses may also explore:

Grants

Crowdfunding

Competitions

Incubators

Accelerators

Pre-orders

Customer deposits

Supplier credit

Partnerships

Grants can be useful, but they are often specific and competitive.

Crowdfunding can work when you have a strong story, audience, product, and campaign plan.

Pre-orders and customer deposits can be powerful because they test demand directly.

Do not assume one funding path is the only path.

Questions to Ask Before Choosing Funding

Before choosing, ask:

Do I want to keep full ownership?

Can the business start small?

Can I get customers before spending heavily?

Would monthly repayment create too much pressure?

Is the business scalable enough for investors?

Do I want outside people involved in decisions?

How much risk can I handle?

What happens if revenue is slower than expected?

Can I prove demand before raising money?

What is the cheapest useful version I can start with?

These questions can help you avoid choosing funding based only on excitement.

Final Thoughts

Funding a business is not only about getting money.

It is about choosing the right kind of pressure.

Bootstrapping gives you control, but may slow growth.

Loans give you capital, but require repayment.

Investors can help you scale, but usually require giving up ownership and accepting growth expectations.

None of these options is automatically better.

The right option depends on the business.

For many beginners, the best first step is to start small, test demand, keep costs low, and learn from the market.

Then, if the business proves itself, funding becomes a tool for growth instead of a gamble.

Choose funding carefully.

Money can help a good business grow.

But it should never be used as a shortcut around testing, planning, and understanding the market.