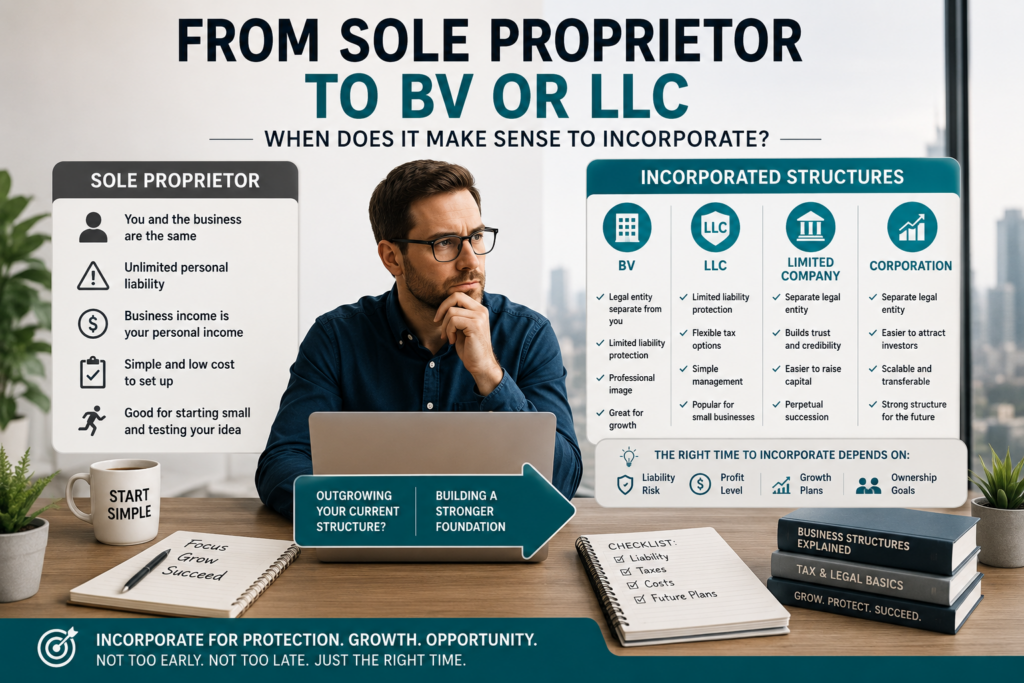

Starting as a sole proprietor is often the simplest way to turn a skill, service, or business idea into income.

There may be fewer formation costs, less administration, and no complicated ownership structure. You can test demand, find your first customers, and learn how the business works before creating a separate company.

But a business can eventually outgrow that simple structure.

As revenue increases, contracts become larger, liabilities grow, and more money remains inside the business, operating personally may expose the owner to risks that were relatively small at the beginning.

That is when entrepreneurs begin asking whether they should move from a sole proprietorship to a structure such as:

- a Dutch BV;

- a US LLC or corporation;

- a UK limited company;

- a Canadian corporation;

- or the local limited-liability equivalent in another country.

The answer is not based on revenue alone.

Incorporation becomes useful when the protection, ownership, continuity, investment, and strategic advantages of a separate company begin to outweigh its additional cost and complexity.

Key Takeaways

- A sole proprietorship is often practical for testing and starting a small business.

- Incorporation creates a legal structure that may be separate from its owner.

- Limited liability can reduce personal exposure, but it is never absolute.

- Tax savings should not be assumed without a country-specific calculation.

- Growing contractual, financial, employment, and product risks can make incorporation more attractive.

- A company structure can make it easier to add shareholders, retain profits, raise capital, or sell the business.

- Incorporating too early can create unnecessary costs and administration.

- The right moment depends on profit, risk, growth plans, location, and personal circumstances.

Affiliate disclosure: This post contains affiliate links. If you make a purchase through one of these links, ProBusinessStrategy may earn a small commission at no extra cost to you. We only recommend tools we genuinely believe in.

What Does It Mean to Incorporate?

Incorporation generally means creating a registered company that has its own legal identity.

Instead of the owner personally entering into every contract, receiving every payment, and carrying every business obligation, the company becomes the contracting party.

A UK limited company, for example, is legally separate from the people who own it. A Canadian corporation can enter contracts and own property in its own name. A Dutch BV also has legal personality and is generally responsible for its own debts.

The terminology differs across countries:

| Country or system | Common simple structure | Common limited structure |

|---|---|---|

| Netherlands | Sole proprietorship or VOF | BV |

| United States | Sole proprietorship | LLC or corporation |

| United Kingdom | Sole trader | Private limited company |

| Canada | Sole proprietorship | Corporation |

| Other jurisdictions | Individual business | Local limited company equivalent |

These structures are not identical. Their tax treatment, governance rules, formation requirements, and liability protection vary.

The common strategic change is that the business begins to exist more clearly as an entity separate from the owner.

Why Many Entrepreneurs Start as Sole Proprietors

A sole proprietorship is usually attractive because it is direct.

The owner and the business are generally not treated as separate legal persons. Business income belongs to the owner, and the owner reports that income through the applicable personal tax system.

This structure can work well when:

- the business is new;

- startup costs are low;

- contracts are small;

- the owner has no employees;

- liability exposure is limited;

- profits are needed immediately for personal living costs;

- the business is still testing its market.

Canada describes the sole proprietorship as the simplest kind of business structure. In the Netherlands, most starting entrepreneurs choose a sole proprietorship, while the UK allows many sole traders to begin trading before completing the more formal process required for a limited company.

Simple does not mean unprofessional.

A sole proprietor can still have:

- a business name;

- a website;

- employees;

- insurance;

- commercial contracts;

- international clients;

- substantial revenue.

Incorporation is therefore not a compulsory graduation ceremony for every successful freelancer.

It is a strategic decision.

The Main Limitation: You and the Business Are Closely Connected

The simplicity of a sole proprietorship also creates its main weakness.

When the owner and the business are not legally separate, the owner may be personally responsible for business debts, claims, damages, and contractual obligations.

In the Netherlands, sole proprietors and partners in a VOF can be personally liable for company debts. UK guidance similarly describes sole traders as personally responsible for business debts.

Consider a freelance designer whose largest risk is a late-paying client. Personal exposure may be manageable.

Now compare that with a company that:

- sells physical products;

- stores customer data;

- signs long-term leases;

- employs staff;

- borrows money;

- manages client funds;

- installs equipment;

- provides regulated advice;

- accepts responsibility for expensive projects.

The potential consequences of a mistake become much larger.

That does not automatically mean incorporation is required. Insurance, contracts, procedures, and professional advice can also reduce risk.

But the larger the possible claim, the more important it becomes to ask whether the owner should remain personally exposed.

Sign 1: Your Liability Risk Is Increasing

Liability is often a stronger reason to incorporate than tax.

A separate company may create a boundary between:

- business assets and personal assets;

- company contracts and personal contracts;

- commercial debts and private finances.

A Dutch BV is generally liable for its own debts, while a Canadian corporation and UK limited company are separate legal entities. US LLC members are also generally not personally liable for the LLC’s debts under the entity structure, although the exact rules depend on state law and individual circumstances.

Limited liability is not unlimited protection.

An owner or director may still become personally liable when they:

- personally guarantee a loan or lease;

- commit fraud;

- act unlawfully;

- mix personal and company finances;

- fail to meet director duties;

- continue trading irresponsibly;

- mismanage the company;

- personally cause damage;

- fail to maintain required formalities.

Dutch official guidance, for example, notes that BV directors can still face personal liability in cases such as mismanagement.

Incorporation should therefore be seen as one layer of protection, not a substitute for responsible management and insurance.

Sign 2: You Are Signing Larger Contracts

A small freelance assignment may create limited exposure.

A contract worth hundreds of thousands may create obligations involving:

- delivery deadlines;

- service levels;

- confidentiality;

- intellectual property;

- data security;

- warranties;

- subcontractors;

- compensation for losses.

Larger clients may also prefer dealing with incorporated suppliers because a company can appear more permanent and structured.

This does not mean that a company is automatically more competent. But some procurement departments, investors, agencies, and enterprise customers have internal requirements that make working with incorporated businesses easier.

When the commercial consequences of a failed contract become too large to carry personally, incorporation deserves serious consideration.

Sign 3: You Want to Leave Money Inside the Business

Many beginners withdraw nearly all business profit to pay personal expenses.

In that situation, creating a company solely for tax reasons may offer little advantage once formation costs, accounting, payroll requirements, and annual compliance are included.

The calculation can change when the business produces more profit than the owner needs personally.

A company may be able to retain part of its after-tax profit for:

- marketing;

- equipment;

- product development;

- hiring;

- investments;

- acquisitions;

- cash reserves;

- future expansion.

This can create more planning flexibility, but the tax consequences differ substantially by jurisdiction.

In the United States, an LLC is not automatically taxed as a corporation. A single-member LLC is generally treated as part of the owner’s tax return unless it elects corporate treatment, while a multi-member LLC is normally treated as a partnership unless it elects otherwise.

In the Netherlands, a sole proprietor pays income tax on business profit, while a BV pays corporate income tax and may create additional taxation when money is paid to the owner. Official Dutch guidance also notes that a BV has higher costs and that the most tax-efficient structure depends on the specific situation.

The correct question is therefore not:

Which structure has the lowest headline tax rate?

It is:

How much money will I personally need, how much will remain in the business, and what is the total tax and administrative cost of each structure?

Sign 4: You Want to Add Owners or Investors

A sole proprietorship belongs to one individual.

That becomes limiting when you want to:

- give equity to a co-founder;

- offer shares to an investor;

- reward a key team member with ownership;

- divide voting and economic rights;

- create a formal succession plan;

- sell part of the company.

A company structure can make ownership more divisible.

Instead of vaguely promising someone “a percentage of the business,” the company can define:

- who owns which shares;

- who has voting rights;

- how profits are distributed;

- what happens when an owner leaves;

- whether shares can be sold;

- how major decisions are approved.

This does introduce more legal work. Shareholder agreements, articles of association, operating agreements, and local company rules may become necessary.

But when ownership is shared, formal structure is usually safer than relying on informal promises.

Sign 5: The Business Must Continue Without You

A sole proprietorship is closely tied to its owner.

That can create problems when the owner:

- becomes ill;

- dies;

- wants to retire;

- sells the business;

- brings in management;

- steps away from daily operations.

An incorporated company generally has continuing legal existence until it is formally dissolved or otherwise terminated. Canada specifically identifies continuous existence as one of the benefits of incorporation.

This can make it easier to build an asset that exists beyond the founder’s personal labour.

That matters when you want to move from:

- freelancer to agency;

- consultant to product company;

- creator to media business;

- sole operator to employer;

- personal income stream to saleable company.

A company does not automatically create a valuable business.

But it can provide a more suitable container for building one.

Sign 6: You Are Hiring People or Using Subcontractors

A sole proprietor can hire employees or contractors in many jurisdictions.

Incorporation is not always legally required.

However, adding people increases operational exposure:

- payroll obligations;

- workplace claims;

- employment disputes;

- errors by team members;

- customer complaints;

- data access;

- intellectual-property questions;

- health and safety responsibilities.

As the business becomes less dependent on one person and more dependent on a team, formal separation between the company and its founder often becomes more valuable.

The decision should be combined with:

- employment contracts;

- contractor agreements;

- payroll compliance;

- insurance;

- data-security policies;

- documented processes.

Creating a company without improving any of these systems provides only partial protection.

Sign 7: You May Sell the Business Later

Selling a sole proprietorship can require transferring individual assets, contracts, customer relationships, intellectual property, inventory, and liabilities.

An incorporated company may sometimes be sold through a transfer of shares, although asset sales are also common.

The Netherlands lists easier business sale as one possible reason for converting a sole proprietorship into a BV. Canada similarly notes that because a corporation owns property separately, a transfer of shares does not itself change ownership of the corporation’s underlying assets.

The right sale structure depends on:

- tax;

- liabilities;

- buyer preferences;

- contractual permissions;

- intellectual property;

- local law.

Still, entrepreneurs planning an eventual exit should think about legal structure long before a buyer appears.

When Incorporation May Be Premature

Creating a company is not automatically a sign of success.

It may be too early when:

- revenue is inconsistent;

- profit is small;

- business risks are limited;

- nearly all income is withdrawn personally;

- the idea is still being tested;

- annual compliance costs would consume a large share of profit;

- the owner does not need investors or partners;

- insurance already covers the main risks;

- the entrepreneur is likely to stop soon.

A company may require:

- registration fees;

- annual filings;

- separate tax returns;

- bookkeeping;

- payroll administration;

- company records;

- separate banking;

- director obligations;

- professional advice.

The UK requires limited companies to keep company and accounting records and to maintain a clear separation between company and personal finances. Dutch BV formation generally involves a civil-law notary, while changing from a sole proprietorship to a BV may also have tax consequences depending on the conversion method.

Paying for a formal structure that provides no practical advantage can weaken a young business rather than strengthen it.

BV, LLC, Limited Company, and Corporation Are Not Interchangeable

Entrepreneurs frequently use these terms as though they describe the same product.

They do not.

Dutch BV

A BV is a private limited company with legal personality. It is generally responsible for its own debts, although directors can still face personal liability in exceptional circumstances.

US LLC

An LLC is formed under state law. Its liability structure and federal tax classification are separate questions. Depending on ownership and tax elections, it may be treated federally as a sole proprietorship, partnership, or corporation.

UK Limited Company

A UK private limited company is legally separate from its owners and is run by directors. It comes with company, accounting, reporting, and tax responsibilities.

Canadian Corporation

A Canadian corporation is a separate legal entity that can own property and enter contracts independently of its shareholders. Incorporation may occur federally or provincially.

The purpose of this article is not to choose between them. It is to recognise when remaining a sole proprietor may no longer support the business you are building.

A Simple Incorporation Decision Framework

Ask these seven questions.

1. What could realistically go wrong?

Estimate the possible financial impact of:

- debt;

- lawsuits;

- failed projects;

- product problems;

- professional mistakes;

- employee claims.

2. Are personal assets exposed?

Determine whether your current structure makes you personally responsible and which risks can be reduced through insurance or contracts.

3. How much profit do you need personally?

Separate revenue from profit and profit from personal cash requirements.

4. Will money remain inside the business?

Retained profit can make company-based planning more relevant.

5. Will ownership change?

Consider co-founders, investors, employees, succession, and a future sale.

6. Can the business support the extra cost?

Include bookkeeping, filings, payroll, advisory fees, insurance, banking, and formation costs.

7. Does the structure support the next three years?

Choose for the business you are realistically building—not for an imaginary multinational company, but also not only for how the business looked on its first day.

How to Prepare Before Changing Structure

Before converting, collect a clear picture of the current business:

- annual revenue and profit;

- personal withdrawals;

- outstanding contracts;

- debt and guarantees;

- equipment and other assets;

- intellectual property;

- employees and contractors;

- insurance;

- tax obligations;

- planned investments;

- ownership plans;

- international activity.

Then compare at least three scenarios:

- remain a sole proprietor;

- incorporate now;

- remain a sole proprietor temporarily and incorporate after reaching a defined trigger.

Useful triggers might include:

- signing a major contract;

- hiring the first employee;

- launching a higher-risk product;

- accepting an investor;

- reaching a sustainable profit level;

- retaining a meaningful amount of cash;

- expanding internationally.

The conversion itself can create tax and administrative consequences. In Canada, a change to a corporation can require a new business number and new tax-program accounts. Dutch authorities similarly recognise several different conversion methods, each with different consequences.

The decision should therefore be planned, not rushed.

Final Thoughts

A sole proprietorship is not an inferior business structure.

For many freelancers, consultants, local service providers, and early-stage entrepreneurs, it is efficient, affordable, and entirely appropriate.

The reason to incorporate is not to look more successful.

It is to solve a real business problem.

That problem may be:

- growing liability;

- retained profit;

- shared ownership;

- outside investment;

- continuity;

- hiring;

- larger contracts;

- eventual sale.

When those factors become important, a BV, LLC, limited company, corporation, or comparable structure may provide a stronger foundation.

But incorporation also creates new responsibilities. The company must be treated as a genuine separate business, with proper records, financial separation, compliance, and governance.

The smartest approach is not to incorporate as early as possible or to remain a sole proprietor for as long as possible.

It is to change structure when the commercial benefits clearly exceed the financial and administrative burden.

Explore the Global Freelancing & Business Structures hub for practical guidance on freelancing, legal risk, company structures, and international growth.

Disclaimer: This article provides general educational information and does not constitute legal, tax, accounting, or financial advice. Business structures and tax consequences differ by country, state, province, and individual circumstances. Consult qualified local professionals before changing legal structure.