Moving a business abroad can sound like the ultimate entrepreneurial upgrade.

A different country may offer lower taxes, easier access to international customers, better investment opportunities, lower operating costs, or a more business-friendly environment. For an online entrepreneur, the idea can seem especially attractive because the company may not depend on a physical shop, warehouse, or local customer base.

But “moving your business abroad” is not one simple action.

You might be considering:

- moving to another country personally;

- registering a new foreign company;

- relocating an existing company;

- opening a foreign branch;

- creating an international subsidiary;

- moving intellectual property or investments;

- operating remotely while keeping the original business;

- or managing a foreign company from your current country.

Each option can produce very different legal, tax, banking, immigration, and administrative consequences.

A company registered abroad is not automatically taxed only abroad. A foreign address does not necessarily change where the company is actually managed. And a lower corporate tax rate can become irrelevant once accounting costs, payroll obligations, withholding taxes, substance requirements, and personal taxation are included.

Moving abroad can be an excellent strategic decision.

It can also create two-country compliance, unexpected tax exposure, and a structure that is more expensive than the business it was meant to improve.

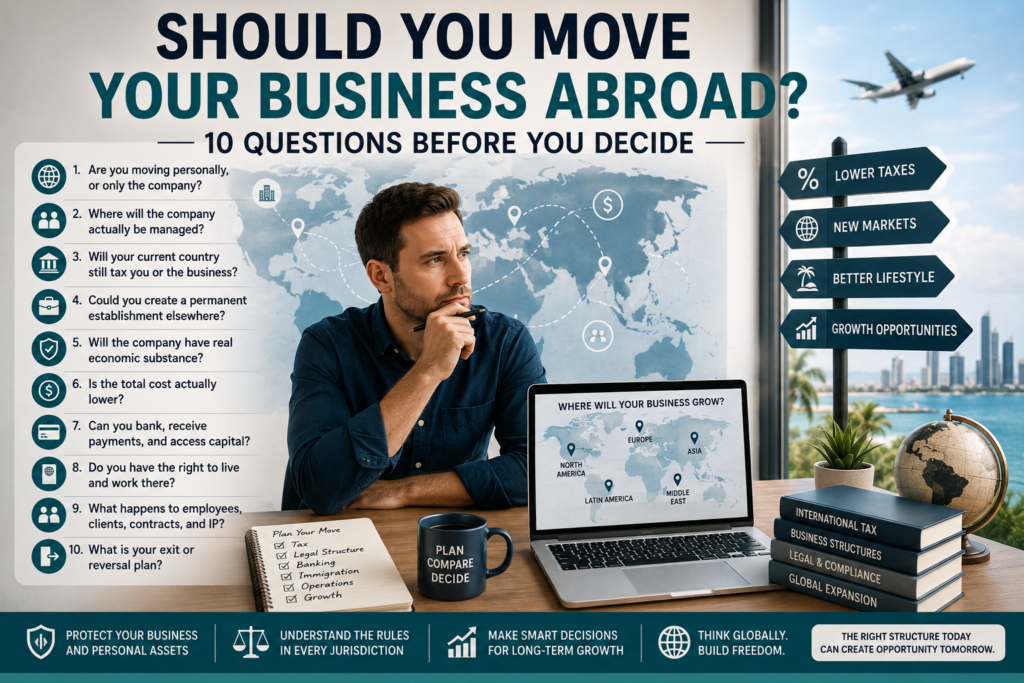

Before making the move, answer these ten questions.

Key Takeaways

- Moving yourself, moving an existing company, and creating a foreign company are separate decisions.

- Company registration does not automatically determine tax residence.

- Where the business is actually managed can be as important as where it is incorporated.

- Working from another country may create a taxable business presence there.

- Tax treaties can reduce double taxation, but they do not eliminate every obligation.

- A foreign structure should have a genuine commercial purpose and sufficient economic substance.

- Banking, payment processing, immigration, staffing, and customer access may matter more than the headline tax rate.

- Moving an existing business can trigger exit taxes or other transfer costs.

- International expansion is usually stronger when driven by markets, operations, investment, or lifestyle—not tax alone.

- Local advice is essential before changing residence, ownership, or company structure.

Affiliate disclosure: This post contains affiliate links. If you make a purchase through one of these links, ProBusinessStrategy may earn a small commission at no extra cost to you. We only recommend tools we genuinely believe in.

What Does “Moving Your Business Abroad” Actually Mean?

Entrepreneurs often use the phrase as if it describes one standard process.

In practice, it can mean several things.

You move, but the company stays

You may continue owning the same company while personally moving to another country.

The business remains registered in its original jurisdiction, but your relocation may affect:

- personal tax residence;

- social-security contributions;

- payroll;

- director compensation;

- company management;

- permanent-establishment exposure;

- immigration and work permissions.

You create a new foreign company

You may keep your existing business and create another company in a different country.

The new company might serve:

- foreign customers;

- a regional market;

- investments;

- intellectual property;

- local employees;

- a specific product or activity.

This creates a group structure rather than relocating the original company.

You open a branch

A branch is generally an extension of an existing company rather than a completely separate business.

It may allow the original company to operate in another country, but it can also expose the main company directly to obligations and liabilities created by the branch.

You create a subsidiary

A subsidiary is normally a separate legal entity owned by the parent company.

This can create clearer separation between activities, but it also introduces additional accounting, tax, governance, and reporting obligations.

You legally convert or relocate the company

In some regions, an existing company may be able to move its registered office or convert into a legal form in another country.

Within the European Union, qualifying companies may use a cross-border conversion to move their registered office to another member state while retaining legal personality rather than dissolving and rebuilding the company from zero. National requirements and protections for shareholders, creditors, and employees still apply.

These routes are not interchangeable. Before comparing countries, first decide what you are actually trying to move.

1. Are You Moving Personally, or Only Moving the Company?

This is the most important distinction.

An entrepreneur can own a company in one country, live in another, serve customers in several more, and use banking or platforms based elsewhere.

That does not mean the entrepreneur can simply choose one country and ignore the others.

You need to identify separately:

- where you personally live;

- where you are personally tax resident;

- where the company is incorporated;

- where the company is tax resident;

- where management decisions are made;

- where employees and contractors work;

- where customers are located;

- where the company has offices or other fixed operations.

Tax residence is determined under each jurisdiction’s domestic rules. In some circumstances, an individual or entity may satisfy the tax-residence conditions of more than one jurisdiction. Tax treaties may then provide procedures for resolving or managing the overlap.

For many entrepreneurs, the real objective is personal relocation rather than corporate relocation.

They may want:

- a different lifestyle;

- better weather;

- lower living costs;

- easier travel;

- a larger entrepreneurial community;

- a residence permit;

- greater personal tax efficiency.

Those can be valid goals. But moving yourself does not automatically move the tax residence or legal obligations of the company.

2. Where Will the Company Actually Be Managed?

A company can be incorporated in one country while being managed from another.

This is where many simple “open a company abroad” strategies begin to break down.

Different countries use different residence tests, but common concepts include:

- incorporation;

- central management and control;

- place of effective management;

- location of key decision-makers;

- location where strategic decisions are made.

UK guidance states that a company may be UK-resident when it is incorporated in the UK or when its central management and control is in the UK. HMRC also emphasises that the location of board meetings can be relevant but is not automatically decisive; the complete facts and actual management must be examined.

Information published through the OECD’s tax-residency resources similarly explains that a company can be considered Dutch tax-resident when its place of effective management is in the Netherlands.

Imagine that you create a foreign company but:

- continue living in your original country;

- make every strategic decision from your home office;

- negotiate all major contracts there;

- control the bank accounts there;

- have no meaningful management abroad;

- use only a registered-address service in the foreign country.

The company may be incorporated abroad, but tax authorities could still examine whether it is effectively managed from your home country.

A local nominee, mailbox, or occasional board meeting does not necessarily change the commercial reality.

Ask:

Where are the important business decisions genuinely made, documented, and implemented?

If the honest answer is still your current country, registering elsewhere may not achieve what you expect.

3. Will Your Current Country Continue to Tax You or the Business?

Moving abroad does not always end existing tax obligations.

Your original country may continue taxing:

- locally sourced income;

- property;

- a remaining permanent establishment;

- dividends or interest;

- capital gains;

- payroll;

- certain company profits;

- assets transferred out of the jurisdiction.

Your personal citizenship can also matter.

US citizens and resident aliens generally remain subject to US tax reporting on worldwide income even while living abroad. Reliefs such as foreign tax credits or the foreign earned income exclusion may be available when the requirements are satisfied, but foreign residence does not automatically end US filing obligations.

Other countries rely more heavily on residence than citizenship, but leaving still requires a proper analysis of:

- the departure date;

- remaining personal ties;

- available housing;

- family location;

- business interests;

- days spent in each country;

- treaty rules.

A structure that looks attractive for one nationality or country of origin may be ineffective for someone else.

This is why international business advice cannot be reduced to:

“Register in Country X and pay only Y percent.”

Your personal circumstances remain part of the calculation.

4. Could You Create a Permanent Establishment in Another Country?

A company does not always need to incorporate a separate subsidiary before becoming taxable abroad.

Business activities can sometimes create a permanent establishment, often shortened to PE.

The precise definition depends on domestic law and the relevant tax treaty, but it generally concerns a sufficiently significant business presence in another jurisdiction.

Possible triggers can include:

- an office;

- a branch;

- a workshop;

- a fixed place of business;

- employees operating from a location;

- a person habitually concluding contracts;

- certain long-term projects;

- in some circumstances, cross-border remote work.

The OECD updated its Model Tax Convention commentary in 2025 to provide additional guidance on when cross-border remote work from a home office may create a taxable business presence. The analysis depends on the specific facts rather than every remote-working arrangement automatically creating a permanent establishment.

Within the EU, the European Commission notes that an SME can become taxable in another member state once its foreign activities create a permanent establishment. That can require the company to comply with more than one national tax system.

This issue can arise even when you did not intend to “move” the company.

For example:

- a founder manages the business from another country;

- an employee permanently works from abroad;

- a sales representative regularly signs contracts locally;

- a company rents a long-term workspace;

- core operations are performed from a foreign location.

International expansion therefore requires an operational map, not merely a list of registered entities.

5. Will the Foreign Company Have Real Economic Substance?

A company should exist for more than obtaining a favourable tax rate.

Economic substance generally concerns whether the company has genuine activity and an appropriate presence relative to what it claims to do.

Depending on the jurisdiction and activity, relevant factors may include:

- qualified local directors;

- employees;

- physical premises;

- operating expenses;

- decision-making;

- equipment;

- records;

- actual commercial activity;

- local management;

- genuine business risk.

The OECD’s work on base erosion and profit shifting is based on the principle that profits should be taxed where economic activities occur and value is created, rather than being artificially shifted to low-tax locations.

Several jurisdictions traditionally associated with international structures have introduced economic-substance requirements, especially for certain geographically mobile activities.

A one-person online business may not need a large foreign office and ten employees. Substance should be proportionate to the activity.

But you should still be able to answer:

- Why does this company exist in that country?

- What activity happens there?

- Who makes decisions there?

- What assets and risks does it control?

- Does the structure match commercial reality?

A structure designed only on paper can create more risk than protection.

6. Is the Total Cost Actually Lower?

A low corporate tax rate is only one line in a much larger calculation.

You may also face:

- company-formation fees;

- annual renewal costs;

- registered-office charges;

- local directors;

- bookkeeping;

- corporate tax filings;

- VAT or sales-tax registration;

- payroll;

- audit requirements;

- legal advice;

- banking costs;

- insurance;

- translation;

- local substance costs;

- withholding tax;

- taxation when profit is distributed personally;

- compliance in your home country.

You should compare total outcomes rather than headline rates.

Calculate:

- profit before tax;

- corporate tax;

- local business costs;

- personal salary taxation;

- social contributions;

- dividend taxation;

- withholding taxes;

- tax in your country of residence;

- available treaty relief;

- annual professional and compliance costs.

A foreign company that saves €8,000 in corporate tax but creates €12,000 in administration, advice, and substance costs is not a tax-saving structure.

Tax is also not the only financial consideration.

A jurisdiction with a slightly higher rate may provide:

- better banking;

- stronger legal protection;

- respected courts;

- easier payment processing;

- better investor access;

- more stable regulation;

- stronger treaty networks;

- greater customer trust.

The cheapest jurisdiction is not necessarily the best business environment.

7. Can You Reliably Bank, Receive Payments, and Access Capital?

A company cannot operate effectively without financial infrastructure.

Before choosing a jurisdiction, investigate whether you can obtain:

- a business bank account;

- payment processing;

- merchant services;

- credit;

- local or international financing;

- investment accounts;

- multiple-currency support;

- transfers to yourself or related companies.

Do not assume incorporation guarantees banking access.

Financial institutions may ask for:

- proof of residence;

- tax identification numbers;

- business plans;

- customer contracts;

- source-of-funds documentation;

- beneficial-owner information;

- local substance;

- transaction forecasts;

- evidence of commercial activity.

Some payment platforms restrict countries, industries, products, or ownership structures. A legally valid company can still be commercially unusable when major payment providers will not support it.

Also consider the company’s reputation with:

- customers;

- suppliers;

- investors;

- affiliate networks;

- advertising platforms;

- marketplaces.

An exotic structure that requires a lengthy explanation during every compliance review may not support the simple global business you intended to build.

8. Do You Have the Right to Live and Work There?

Owning a company does not automatically give you the right to live or work in the country where it is registered.

These are separate systems:

- company law determines whether you can form or own the entity;

- immigration law determines whether you may enter, reside, and work;

- tax law determines which income and entities are taxable;

- employment and social-security law determine additional obligations.

Within the EU, EU citizens generally have broad rights to live and work in other member states, subject to applicable administrative conditions. Non-EU nationals may need residence and work permission based on national and EU rules.

Outside such free-movement arrangements, an entrepreneur may require:

- an investor visa;

- entrepreneur visa;

- digital-nomad visa;

- residence permit;

- work authorisation;

- proof of income;

- health insurance;

- a local address;

- minimum investment.

A digital-nomad visa may allow remote work but may not permit you to trade locally, hire staff, or manage certain kinds of domestic business.

Check what the permission actually allows—not only how it is advertised.

9. What Happens to Employees, Clients, Contracts, Data, and Intellectual Property?

A company is more than its registration certificate.

Moving or restructuring it can affect existing relationships and assets.

Employees

Hiring or relocating staff can create:

- payroll registration;

- local employment rights;

- social-security obligations;

- pension requirements;

- immigration issues;

- workplace insurance;

- termination protections.

Within the EU, employers hiring in another member state may need to register with local authorities and comply with local labour, tax, and social-security obligations.

Clients and contracts

Review whether contracts allow:

- assignment to a new company;

- changes of jurisdiction;

- cross-border data processing;

- new banking details;

- subcontracting;

- transfer of intellectual property.

Some customers may need to approve the change. Others may need to run a new supplier or compliance review.

Intellectual property

Determine who owns:

- trademarks;

- domain names;

- software;

- designs;

- written content;

- customer databases;

- licences.

Transferring intellectual property to a foreign company can have valuation and tax consequences. It should not be moved informally.

Data

Customer and employee data may be subject to restrictions on international transfer, storage, access, and processing.

Licences and permits

A licence issued to one company or in one country may not transfer automatically.

The more operationally developed the existing business is, the more carefully the move must be planned.

10. What Is Your Exit or Reversal Plan?

Entrepreneurs often plan how to enter a foreign jurisdiction but not how to leave it.

Ask what happens when:

- the country changes its tax rules;

- annual costs rise;

- your visa expires;

- banking becomes difficult;

- the business model changes;

- you return home;

- you sell the company;

- you want to close the structure;

- you move to a third country.

Closing or relocating a company can involve:

- liquidation;

- final tax returns;

- creditor procedures;

- asset transfers;

- employee termination;

- contract migration;

- capital-gains tax;

- exit taxation;

- deregistration costs.

For example, Dutch official business guidance explains that moving a company to another EU country can trigger a final tax settlement or exit taxation, with rules governing immediate or deferred payment.

Your original country may also tax unrealised gains when assets, residence, or business activities leave its tax jurisdiction.

A good international structure should be workable not only when created but also when changed or dismantled.

When Moving a Business Abroad Can Make Sense

International relocation or expansion can be commercially strong when it supports a genuine objective.

Examples include:

Accessing a larger market

A local presence may improve:

- customer trust;

- distribution;

- sales;

- partnerships;

- public procurement;

- payment options;

- local marketing.

Hiring talent

The country may offer better access to specialised employees, contractors, universities, or technical communities.

Raising investment

Investors sometimes prefer familiar legal structures and jurisdictions with established corporate law.

Improving operations

You may benefit from:

- better infrastructure;

- logistics;

- manufacturing;

- digital services;

- lower operating expenses;

- stronger supplier networks.

Protecting or organising assets

A group structure may create clearer separation between:

- trading activities;

- intellectual property;

- property;

- investments;

- regional operations.

Supporting a genuine relocation

When the founder really moves, manages the business locally, builds relationships, and develops operations there, the structure has a stronger commercial foundation.

Creating regional expansion

A subsidiary or branch may help serve a new geographic market without moving the entire original company.

Tax efficiency can be part of the decision, but it is strongest when it follows genuine commercial activity rather than replacing it.

Weak Reasons to Move Your Business Abroad

Be cautious when the main reason is:

- a social-media video promising zero tax;

- one attractive headline rate;

- frustration with one bill or government policy;

- the belief that online businesses are not taxable anywhere;

- the assumption that a foreign LLC automatically protects everything;

- advice that ignores your residence and nationality;

- a desire to hide income or ownership;

- copying a structure built for a much larger company.

Another warning sign is when the adviser explains only how to open the structure but not:

- how it is taxed;

- how you will bank;

- where management takes place;

- what filings remain due at home;

- how money reaches you personally;

- what happens when you close it.

Formation is usually the easiest part.

Living with the structure is what matters.

A Practical International Expansion Framework

Before moving, prepare a written comparison.

Current situation

Document:

- personal residence;

- citizenship;

- current company structure;

- annual revenue and profit;

- customer locations;

- employees and contractors;

- business assets;

- current tax burden;

- personal cash requirements;

- growth plans.

Proposed structure

Clarify:

- which entity will exist;

- where it will be incorporated;

- where it will be managed;

- who will own it;

- where banking will take place;

- where employees will work;

- what commercial activity happens locally;

- how profit reaches the owner.

Total annual cost

Include:

- tax;

- salary;

- dividends;

- social security;

- bookkeeping;

- legal advice;

- banking;

- insurance;

- residence costs;

- substance requirements;

- home-country compliance.

Risk analysis

Examine:

- dual tax residence;

- permanent establishment;

- personal liability;

- controlled foreign company rules;

- withholding tax;

- exit taxation;

- immigration;

- banking;

- reputational risk.

Three scenarios

Compare:

- keep the existing structure;

- add a foreign branch or subsidiary;

- relocate the company and/or founder.

The third option is not automatically best merely because it is the most dramatic.

Final Thoughts

Moving a business abroad can create real advantages.

It may open markets, improve access to talent, support investment, create a better personal lifestyle, or provide a stronger international structure.

But registering a company in another country is not the same as relocating a functioning business.

The important questions are:

- where you live;

- where decisions are made;

- where value is created;

- where people work;

- where customers are served;

- where the company has a taxable presence;

- and how the structure operates in reality.

A foreign company should be treated as a genuine business structure, not a decorative address attached to an operation that remains entirely somewhere else.

The smartest international entrepreneurs do not start by asking:

Which country has the lowest tax rate?

They ask:

Which structure best supports the business, lifestyle, customers, risks, investments, and long-term plans I am actually building?

When the commercial reasons are strong and the structure reflects reality, international expansion can create freedom and opportunity.

When the plan exists only on paper, the promised simplicity can quickly become expensive complexity.

Explore the Global Freelancing & Business Structures hub for guidance on freelancing, legal risk, business structures, and international growth.

Disclaimer: This article provides general educational information and does not constitute legal, tax, immigration, accounting, or financial advice. International rules differ by jurisdiction and individual circumstances. Consult qualified advisers in every relevant country before relocating yourself, your company, or business assets.