Freelancing gives people the freedom to choose clients, set prices, organise their work, and build an independent business.

But calling someone a freelancer does not automatically make that person legally self-employed.

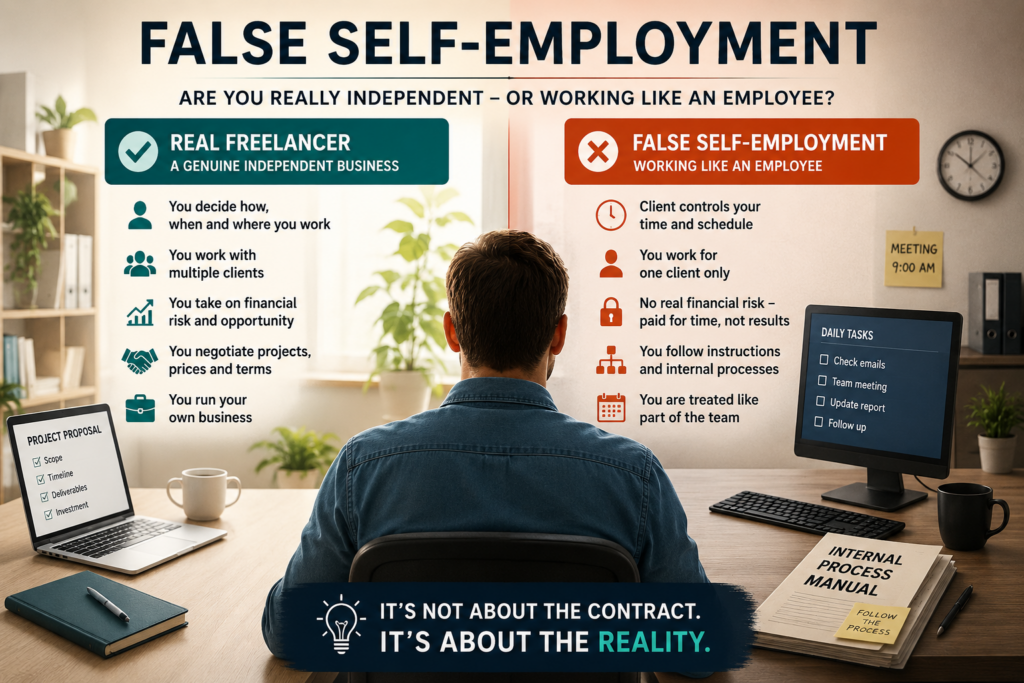

A working relationship may be presented as freelance while operating much more like regular employment. The freelancer sends invoices and pays their own taxes, but the client decides when, where, and how the work must be performed.

This situation is commonly known as false self-employment, bogus self-employment, or worker misclassification.

The exact legal definition differs between countries. However, the central question is usually similar:

Is this person genuinely operating an independent business, or are they economically and operationally dependent on one organisation?

Understanding that distinction is essential for freelancers, online contractors, platform workers, consultants, and the businesses that hire them.

Key Takeaways

- A freelance contract does not automatically prove self-employment.

- Authorities generally examine how the relationship works in practice.

- Control, financial risk, independence, and economic dependence can all matter.

- Working for one client does not automatically make someone an employee.

- Having several clients does not automatically prove genuine independence.

- False self-employment can create financial and legal consequences for both parties.

- The strongest protection is to build a working relationship that functions like a real business arrangement.

Affiliate disclosure: This post contains affiliate links. If you make a purchase through one of these links, ProBusinessStrategy may earn a small commission at no extra cost to you. We only recommend tools we genuinely believe in.

What Is False Self-Employment?

False self-employment occurs when someone is officially treated as an independent contractor but works under conditions that more closely resemble employment.

The person may:

- register as self-employed;

- sign a contractor agreement;

- send invoices;

- arrange their own tax payments;

- receive no holiday pay or employment benefits.

But beneath that formal structure, the client may exercise significant control over the person’s work.

For example, the client might determine:

- the worker’s schedule;

- where the work must be performed;

- the exact methods that must be used;

- which assignments must be accepted;

- how much the worker is paid;

- whether the worker may serve other clients;

- when the relationship can be ended.

Several governments explicitly state that the practical working relationship matters more than the title used in a contract. The Dutch government defines false self-employment as hiring someone as a self-employed professional when the relationship is actually employment. UK guidance similarly says that contractual wording is not conclusive when it does not correspond with reality.

Why Businesses Use Freelance Arrangements

There are many legitimate reasons to hire freelancers.

A company may need:

- specialist knowledge for one project;

- temporary capacity;

- help during a seasonal peak;

- services that are not required every day;

- access to international expertise;

- support without creating a permanent internal role.

These are normal commercial relationships.

Problems arise when a company uses a freelance agreement mainly to obtain employee-level labour without accepting employee-level responsibilities.

Depending on the country, an employer may otherwise have responsibilities involving:

- minimum wages;

- payroll taxes;

- social-security contributions;

- paid holidays;

- sick leave;

- pension contributions;

- working-time protections;

- dismissal procedures;

- unemployment or workplace insurance.

Misclassification can therefore reduce costs for the hiring business while transferring risk to the individual performing the work.

In the United States, the Department of Labor warns that workers misclassified as independent contractors may lose protections such as minimum wage and overtime pay.

A Contract Is Not Enough

One of the most common misunderstandings is that a well-written freelance contract determines someone’s legal status.

It does not.

A contract is important because it records the intentions, services, responsibilities, and commercial terms agreed by the parties. But authorities and courts may look beyond the document.

Imagine that a contract says:

The contractor is free to determine how and when the services are performed.

In practice, however, the person must:

- work from 9:00 a.m. until 5:00 p.m.;

- attend daily employee meetings;

- request permission for time off;

- follow instructions from a manager;

- use only company equipment;

- remain continuously available;

- obtain approval before accepting other clients.

The daily reality conflicts with the written agreement.

In that situation, repeatedly writing “independent contractor” into the contract will not necessarily protect either party.

The UK government states that status is governed mainly by the reality of the relationship. The US Department of Labor likewise says an independent contractor agreement does not override economic dependence when evaluating status under federal wage law.

Common Signs of False Self-Employment

No single test works in every country. Even within one country, different rules may apply for employment rights, tax, social security, or a particular industry.

Still, several recurring factors appear in classification tests around the world.

1. The Client Controls How the Work Is Performed

Independent professionals normally decide how to deliver their services.

A client can still set:

- deadlines;

- quality standards;

- project objectives;

- safety requirements;

- legal or technical specifications.

That is normal.

The relationship starts to look more like employment when the client controls the person’s working methods in detail.

Examples include:

- constant supervision;

- mandatory step-by-step instructions;

- fixed internal procedures for ordinary work;

- regular performance management;

- permission requirements for routine decisions.

The more operational control the client exercises, the harder it may be to demonstrate genuine independence.

2. The Freelancer Cannot Reject Assignments

A real business can normally decide whether to accept a customer or project.

A freelancer may agree to complete all work included within an existing project. But if the client can continuously assign new tasks and the freelancer is expected to accept them, the arrangement may look more like employment.

This is especially relevant when the client is also expected to keep offering work indefinitely.

The ability to negotiate, accept, decline, or separately price assignments can support genuine commercial independence.

3. The Client Determines the Schedule

Working agreed hours does not automatically create employment.

A photographer must arrive when an event begins. A consultant may need to join a scheduled meeting. A restaurant contractor may need to perform services while the location is open.

Timing becomes more concerning when the person is placed into a permanent employee-style schedule with little control over availability.

Questions include:

- Can the freelancer choose when to work?

- Can assignments be refused?

- Is attendance monitored like employee attendance?

- Must permission be requested for time away?

- Is the person expected to remain available every week?

The complete context matters.

4. The Freelancer Has No Real Financial Risk

Independent businesses can make profits, but they can also lose money.

A freelancer may invest in:

- equipment;

- software;

- training;

- advertising;

- insurance;

- subcontractors;

- office space;

- transportation.

They may also quote a fixed price and earn more by working efficiently—or earn less if the project takes longer than expected.

Someone who receives a fixed amount for every hour worked, makes no investment, cannot negotiate rates, and carries no meaningful commercial risk may look more like a worker than an independent business owner.

Under the US federal economic-reality approach, the ability to earn a profit or suffer a loss through managerial skill and investment is one of the factors used to distinguish independent business activity from economic dependence.

5. The Person Is Integrated Into the Client’s Business

A freelancer can work closely with a client without becoming an employee.

However, risk may increase when the freelancer becomes almost indistinguishable from internal staff.

Examples include:

- using an employee job title;

- appearing on the internal organisation chart;

- managing employees as a permanent department head;

- receiving employee benefits;

- using a company email address without any external-business identity;

- performing an indefinite internal role;

- being presented to customers as a permanent staff member.

A specialist delivering a defined external service is generally easier to distinguish from an employee filling a permanent operational position.

6. The Relationship Is Indefinite

Long-term client relationships are not automatically false self-employment.

Successful freelancers often serve the same customers for many years.

The concern is not simply duration. It is whether the relationship has become a permanent job without the formal protections of employment.

Compare these situations:

Independent relationship:

A marketing consultant completes several separately scoped campaigns for the same client over three years.

Potentially employee-like relationship:

A person works every weekday as the company’s marketing manager, reports to a director, follows an internal schedule, and has no meaningful ability to serve other clients.

Both relationships may be long-term, but their commercial substance is different.

7. The Freelancer Is Economically Dependent on One Client

Receiving most of your income from one client can increase risk, but it is not automatically decisive.

A new freelancer may begin with one major customer. A consultant may temporarily focus on one large project. A specialist may accept an intensive six-month assignment.

The stronger question is whether the person is genuinely in business for themselves.

The US Department of Labor describes the distinction as one between a person who is economically dependent on an employer and someone operating an independent business.

Relevant questions include:

- Does the freelancer market services to other customers?

- Can they negotiate prices?

- Are they free to accept other work?

- Do they have their own commercial identity?

- Can their business continue when this client leaves?

- Do they make independent business decisions?

Dependency should therefore be evaluated as part of the complete relationship.

What False Self-Employment Is Not

Because the topic creates anxiety, it is equally important to understand what does not automatically prove misclassification.

Working for One Client

One client is a risk factor, not an automatic verdict.

The nature of the work, level of control, duration, commercial risk, and wider business activity must also be considered.

Performing the Same Work as Employees

Doing similar work does not always mean the person has the same legal status.

Two people may perform comparable tasks but operate under different conditions. One may follow an employment schedule under management control. The other may provide a defined specialist service through an independent business.

Working at the Client’s Location

Some services must be performed at a specific location.

Examples include:

- event photography;

- equipment installation;

- building maintenance;

- hospitality services;

- on-site consulting;

- technical inspections.

Location is only one part of the assessment.

Charging by the Hour

Hourly pricing is widely used by legitimate consultants, lawyers, designers, developers, and other professionals.

It may be considered alongside other circumstances, but hourly billing alone does not automatically create employment.

Using a Freelance Platform

Finding work through a platform does not automatically make someone an employee or a genuine entrepreneur.

The relevant question is how much control the platform or client exercises over the relationship.

The EU Platform Work Directive focuses on correctly determining the status of people whose work is organised through digital labour platforms. It also addresses algorithmic monitoring and automated decisions that can significantly affect workers.

Why False Self-Employment Matters to Freelancers

Some people initially prefer being classified as self-employed because they value flexibility or believe they will earn more.

But a misclassified worker may carry the disadvantages of self-employment without receiving genuine entrepreneurial freedom.

They may have:

- no paid holidays;

- no sick pay;

- no unemployment protection;

- no employer pension contributions;

- no minimum income guarantees;

- limited protection against dismissal;

- responsibility for their own taxes and insurance.

At the same time, they may still be controlled like an employee.

That is often the central injustice of false self-employment:

The individual carries the risks of business ownership without receiving the control or opportunity that normally comes with running a business.

Misclassification can also create uncertainty later. A freelancer may need to pursue unpaid employment rights, correct tax records, or defend their status during an investigation.

Why It Matters to Clients

Businesses also face substantial risks.

Depending on local law, reclassification may result in:

- unpaid payroll taxes;

- social-security contributions;

- pension liabilities;

- holiday-pay claims;

- minimum-wage claims;

- overtime claims;

- interest and penalties;

- employment-rights disputes;

- reputational damage.

The Dutch government states that clients and freelancers are jointly responsible for choosing a contract that matches how the work is actually performed. If a freelance relationship is found to be employment, the client can face payroll-tax obligations as well as employment and pension-law risks.

Avoiding the issue is therefore not a sensible risk-management strategy.

A Simple False Self-Employment Self-Check

This checklist cannot determine legal status, but it can reveal areas that deserve closer attention.

Ask yourself:

Control

- Who decides how the work is performed?

- Can the client give employee-style instructions?

- Is the freelancer closely supervised?

Time and availability

- Who sets the working schedule?

- Can the freelancer reject assignments?

- Must permission be requested for time away?

Pricing and financial risk

- Can the freelancer negotiate rates?

- Does the freelancer invest in the business?

- Can the project produce a profit or loss?

Clients and market activity

- Can the freelancer work for other clients?

- Are services actively marketed?

- Does the freelancer have a separate business identity?

Integration

- Is the person filling a permanent internal role?

- Are they managed like ordinary staff?

- Are customers told that the freelancer is an employee?

Duration and purpose

- Is there a clearly defined project or service?

- Does each assignment have an identifiable scope?

- Has a temporary project gradually become a permanent job?

The more the arrangement resembles internal employment, the more important it becomes to obtain professional advice.

How Freelancers Can Strengthen Genuine Independence

A freelancer should not create artificial appearances merely to avoid employment law. The objective is to build a business that is genuinely independent.

Practical steps include:

Define services clearly

Sell specific services, projects, or outcomes instead of offering unlimited general availability.

Negotiate commercial terms

Discuss scope, price, delivery, revisions, payment, and responsibilities as one business dealing with another.

Maintain a separate business identity

Use appropriate invoices, business records, marketing materials, and communication channels.

Preserve the freedom to serve other clients

Avoid unnecessary exclusivity unless there is a clear commercial reason and appropriate compensation.

Build more than one source of business

Develop direct clients, referrals, partnerships, platforms, content, or repeatable service packages.

Record what was agreed

Use written contracts and project scopes that reflect the actual working relationship.

Review long-term arrangements

A legitimate freelance project can gradually change. Review relationships that become longer, more integrated, or more controlled than originally intended.

When Employment May Be the Better Structure

Not every working relationship should be forced into a freelance model.

Employment may be more appropriate when a business needs someone to:

- fill an ongoing internal position;

- work a fixed weekly schedule;

- follow continuous management instructions;

- remain personally available;

- perform tasks assigned as needs arise;

- represent the company as part of its regular workforce.

This does not mean employment is inferior to freelancing.

It is simply a different structure with different rights, responsibilities, risks, and advantages.

Trying to disguise a regular position as freelance work can create uncertainty for everyone involved.

Final Thoughts

False self-employment is not defined by one clause, one invoice, one client, or one registration document.

It is determined by the complete working relationship.

The central distinction is between:

- someone who genuinely operates an independent business; and

- someone who carries a freelance label while remaining controlled and dependent like an employee.

For freelancers, the solution is not to manufacture superficial signs of entrepreneurship. It is to develop real commercial independence through clear services, decision-making authority, market activity, financial responsibility, and proper business organisation.

For clients, the solution is not to avoid every freelancer. It is to use freelance relationships for genuinely independent services and employment structures for roles that require employee-level control.

Rules differ between countries, and classification can depend on employment, tax, social-security, and industry-specific law. But one principle appears repeatedly across jurisdictions:

What happens in practice is more important than what the relationship is called.

Understanding that principle helps freelancers protect their independence and helps businesses use flexible expertise without turning legitimate contracting into hidden employment.

Explore the Global Freelancing & Business Structures hub for more guidance on freelancer risk, business structures, and international growth.

Disclaimer: This article provides general educational information and does not constitute legal, employment, or tax advice. Classification rules differ by country and individual circumstances. Seek qualified local advice when assessing a specific working relationship.